At a certain age, you start to think that you’re doing it wrong if you’re still paying rent. Maybe it’s something your dad said, or maybe it’s the fact that everyone else your age seems to be getting married and settling down.

Renting, it seems, is less mature and responsible than owning.

But it’s not.

At least not always. If fact, depending on your circumstances, renting might actually be the more fiscally responsible thing to do.

In this article, we’ll approach the rent vs. buy question from a different angle.

Asking yourself whether you should rent or buy is the wrong question. The question you should really be asking yourself is this:

How do I want to live my life?

The difference between “Should I rent or should I buy a house?” and “How do I want to live my life?” is that the second question is much more holistic. Renting and buying are just two ways to pay for housing. You’re only looking at a very small piece of the puzzle.

If you answer the question “How do I want to live my life?” fully, then the rent vs. buy question will answer itself.

Here are some questions you can ask to help you reach that conclusion.

What are my financial goals?

Most people start and end their decision-making process here. The reason they do that is because, from a financial perspective, it appears that you can do the math and get a clear-cut answer.

That’s sort of true.

For the sake of this data point, let’s suss out the financial part of renting vs. buying.

And then I’ll proceed to tell you why it doesn’t matter.

True and False: Paying for Rent is Throwing Money Away

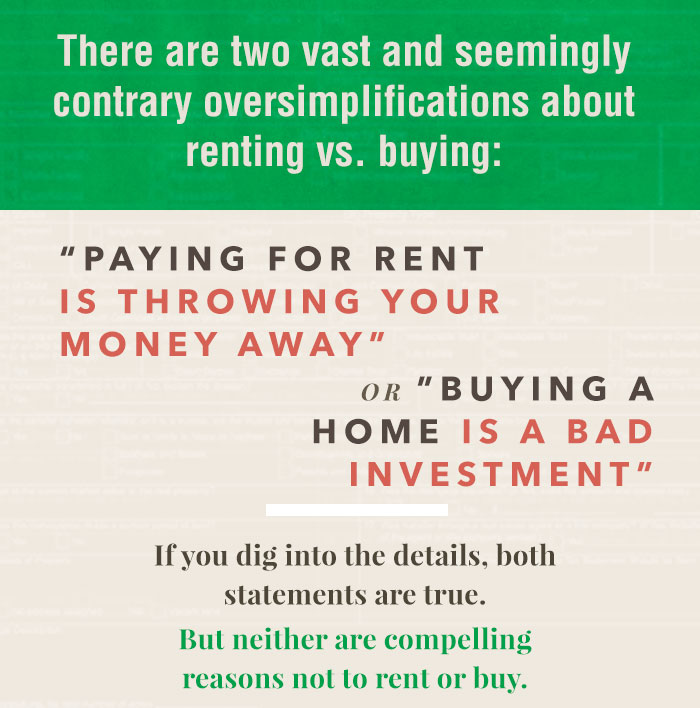

There are two vast and seemingly contrary oversimplifications about renting vs. buying:

- Paying for rent is throwing your money away

- Buying a home is a bad investment

If you dig into the details, both statements are true. But neither are compelling reasons not to rent or buy.

Let’s get a bit more nuanced.

When people say that renting is throwing money away, what they mean is that you’re not building equity. Every time you make a mortgage payment, you own a little bit more of your home. Meanwhile, after paying rent for 30 years you own as much nothing as you did 30 years ago. True.

But not as important as you may think.

Turns out that when you buy a home with a mortgage, you’re renting, too. As this video from Money School puts it, instead of renting space from a landlord, you’re renting money from a bank.

For the first five years, payments toward your principal will be a tiny sliver of your monthly mortgage payment. The rest of it will go toward insurance, taxes, and interest.

Consider interest the rent you pay on borrowing money.

Sometimes, people refer to this breakdown of Principal, Interest, Taxes, and Insurance by the acronym “PITI” as in “I PITI the fool who thinks buying a home is always a smart investment.” On a 30-year mortgage, your first 180 or so mortgage checks will go more towards interest than paying down your principal.

Let’s say you put $20,000 down on a $320,000 home and get a mortgage for the remaining $300,000. For a 30-year fixed rate mortgage at 3% with a principal of $300,000, your monthly mortgage payment will be $1,264.81. You’ll be paying more interest than principal for the first five years. Your total payments will be $75,888.60 after five years, and you’ll only have built $33,280.77 in equity beyond your $20,000 down payment. And that’s not counting taxes, insurance, and closing costs.

But wait, you say. Doesn’t the value of my home appreciate?

Yes, it does, usually. Over time, home values do tend to go up. Most estimates peg the historical home appreciation rate in the U.S. at around 3.5%.

So, let’s say you do turn around and sell your house after five years assuming 3.5% growth with compounded interest at $380,060 versus the $320,000 you paid.

| $380,060 | Sales Price |

| -$266,720 | Mortgage Payoff |

| -$22,803 | Real Estate Agent Commission (6%) |

| -$75,888 | Mortgage Payments to Date |

| $14,649 | Proceeds |

After five years, you end up getting less than your $20,000 down payment back.

What about after 10 years, assuming a 3.5% home appreciation value?

| $423,179 | Sales Price |

| -$228,059 | Mortgage Payoff |

| -$25,390 | Real Estate Agent Commission (6%) |

| -$151,777.20 | Mortgage Payments to Date |

| $17,953 | Proceeds |

Still not too good. Let’s do one more calculation, taking it all the way to 30 years.

| $842,038.11 | Sales Price |

| $0 | Mortgage Payoff |

| -$50,522.29 | Real Estate Agent Commission (6%) |

| -$455,332.36 | Mortgage Payments to Date |

| $336,183.46 | Proceeds |

Now we’re getting somewhere. However, your proceeds amount to about a 1.58% return (You paid the bank a total of $455,332 + $20,000 down payment + $50,522 in agent commission and sold at $842,038).

Could you have gotten a better return if you invested your money elsewhere? Some would say yes. You could buy an index fund and (probably) get a steady 8% to 9% return. And you won’t have to replace the roof or repave the driveway or repair the foundation on an index fund.

This is why they say buying a home is a bad investment. Unless your local housing market booms or you put some sweat equity into structural changes of your home, you’ll earn a meager return on the value of your home, and you’ll have to pay all the transactional costs of buying and selling real estate.

But this doesn’t mean buying a home is a bad purchase.

After all, the reason we buy homes isn’t to make money off them. We buy houses to live in them.

So, don’t think about your house as a big investment. Don’t worry too much about how much profit you’re going to make in 30 years. Instead, consider this: what you’re purchasing is ownership of your home. You may be paying more than a renter over the course of the next five years, but a renter can’t have a cat, can’t paint his walls, can’t drill holes in the brick over his fireplace to mount a 4K TV, can’t convert the basement into a bowling alley…you get the picture.

All that’s not to say that you should ignore the financial side of things. Instead, recognize that the value of your home is one of your assets, but also one of your liabilities. Hopefully, it’s not your only asset (we call that being “house poor”). The question you need to be asking yourself on the financial side of things is this:

Where do I want to be 5, 10, 15, or 30 years from now?

Am I saving up to seed a business? Buy a boat? Retire by 55? Put a kid through college? Put three kids through college?

Then, you need to ask yourself (or your financial planner):

What are my options for getting there?

Investing in the home you live in is one option you should consider as part of your diversified portfolio. But it’s not the only option, and in some cases, it’s not the best option. Tying up your cash in a mortgage rather than putting it toward another investment is what they call “opportunity cost.” Are there better opportunities?

Do that work and put a pin in it. There are more items to consider.

Do people really make more money investing in stocks, bonds, and mutual funds than buying houses?

In theory, if you choose to rent instead of buy, you can take the money you’d save on a down payment and invest it elsewhere to try to beat the 3.5% average home appreciation rate.

But really, no one does that. At least not 100%.

In practice, most renters aren’t disciplined enough to actually invest dollar-for-dollar what they would’ve put toward a mortgage. They end up spending it on emergencies, student loans, trips to Europe, etc., for better or worse.

If nothing else, the threat of losing your home if you don’t make mortgage payments is a great motivator to set money aside for later. Think of it like a piggy bank with a picket fence.

Tip: If you have a couple thousand of extra cash burning a hole in your pocket and don’t want to buy a house, use it to max out your employer-matched 401(k) contribution each year. If your employer matches up to 6% of your $100,000 salary, then that’s $6,000 of free money you can get every year. And free money is a 100% return.

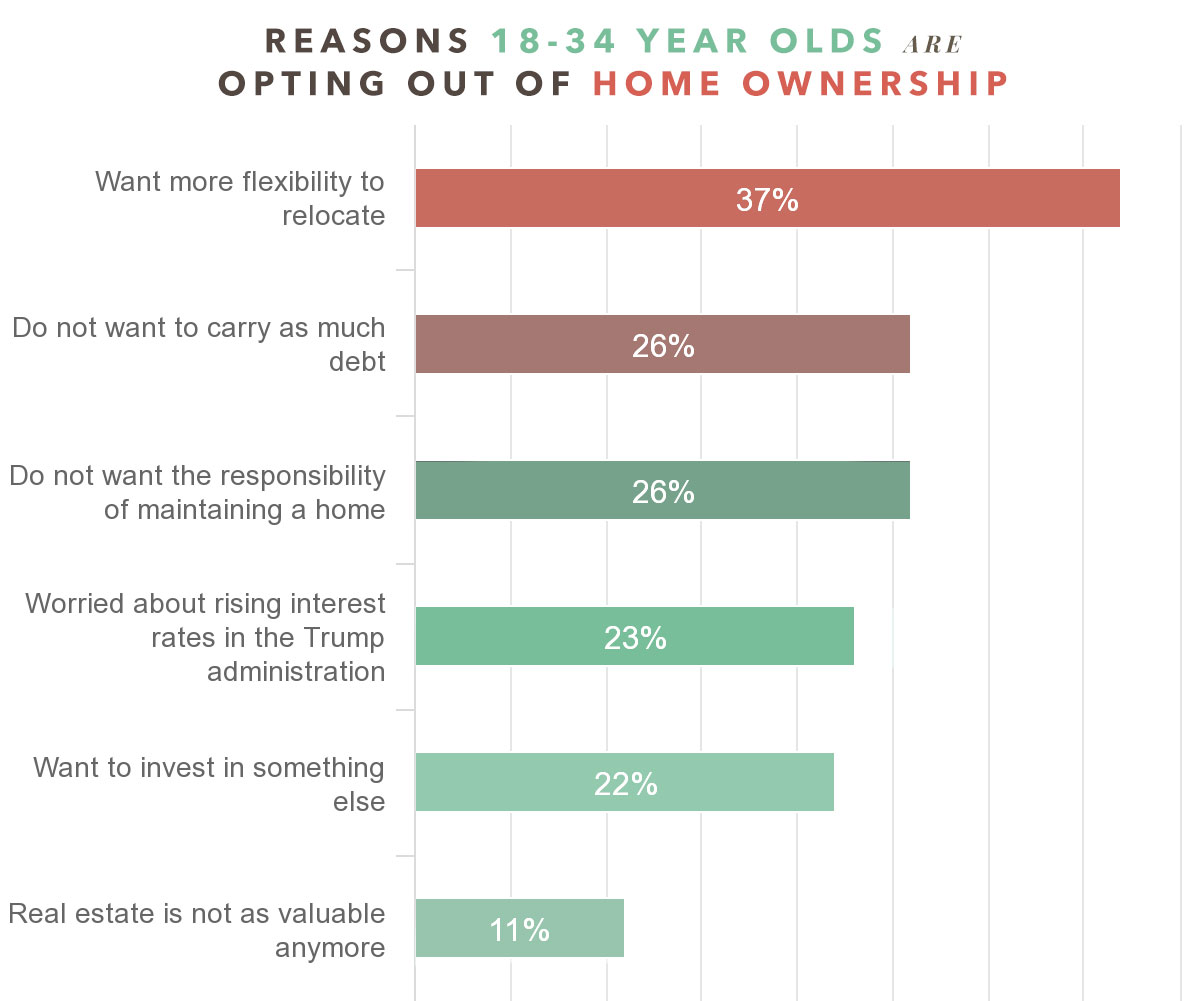

Younger consumers and those in the West are most likely to wait to purchase a home. In fact, 34% of consumers ages 18-34 say they will opt-out of homeownership according to a recent study by Experian.

Where do I want to work? And how far will I drive?

According to a study by LinkedIn, job-hopping in the first five years after graduation has nearly doubled in the last 20 years. We don’t have to get into the reasons why, but suffice to say: if you are young and ambitious, opportunity may come knocking, calling you away to another part of town or another part of the globe.

If you need to sell your home during a market downturn, then you may be forced to take a big loss. If you rent your home and you need to break a lease, you can typically work things out with your landlord as long as you’ve been a good renter and give ample notice. There’s a layover in both situations, but down markets can last years while the end of your lease is probably going to be a matter of months.

Once we decide what zip code you’re in, it’s time to think about where your house is in relation to your job. Face it: most jobs are going to be in city centers, but most affordable homes are going to be in the suburbs. Take some time to think about this critically. Yes, you get the fenced in yard and the 2-car garage. But you also sign yourself up for a 40, 60, or 80 minute commute. There are monetary costs associated with commuting, but the biggest loss is the time spent wasting your life sitting in a car in traffic.

If you’ve been dead set on buying a house, just indulge me for a second and research the prices of rentals closer to the city center where you work. Look at places that allow you to commute by foot, train, or bike. Take a look at the amenities that the rental property has. Consider the parks, the restaurants, the nightlife, and all the other cultural and commercial offerings living in the area will afford you.

Comparing renting a home in the city to buying a home in the suburbs isn’t really the same thing. What you should be doing instead is comparing buying a home in the city center to renting a home in the city center. Buying downtown is usually prohibitively expensive. But if living there is important to you, then the rent vs. buy decision just made itself for you.

On the other hand, buying a home gives you access to some neighborhoods that you can’t rent in. Homeowner associations and condo owner associations often try to discourage or restrict leasing of properties in a neighborhood, since the perception is that owners have a bigger stake in preserving the community than renters.

If your heart is set on an area, you may be forced to rent or buy accordingly.

What do I want to do when I’m not working?

Owning a home means you have to maintain it. This isn’t necessarily a bad thing. A lot of the pride of homeownership comes with using your skills to improve and repair it rather than relying on your landlord and his handyman. If the thought of spending a weekend installing light fixtures or manicuring a lawn or finishing a basement sounds appealing to you, then home ownership is for you. If you are this person, you didn’t need to read this paragraph to understand that. Your hands have been itching to pick up a hammer for years.

This is more for the people who might not have realized how much they’ll hate picking up all the responsibilities that the landlord took care of before. The rule of thumb is that you should set aside 1% of the purchase price of a home a year for home repairs and maintenance. That can really add up, which is why most homeowners tackle simple jobs on their own.

But “simple” doesn’t always mean quick. As a homeowner, you’ll find yourself reserving weekends for home projects. And even if you don’t take it on yourself, you still have to put in the time to find, vet, schedule, and supervise a contractor to do the job.

It’s significantly more involved than texting your landlord when the toilet clogs. For some, this is part of the joy of homeownership—having a hand in physically maintaining and improving your home. For others, it can be a major time and money suck that they resent.

What will my family look like in five years? Ten years?

The other big motivator for moving beside career is family. Where you want to live when you are single without kids will be much different than where you want to live when you’ve got 2.5 kids and a dog and a cat. While no one can predict if and when they’ll meet the one and start procreating, you should at least consider the possibility.

This certainly doesn’t mean you have to rent until you’re hitched. It just means you need to have a plan for what happens in the next five or ten years if the size of your family changes.

Will you be moving closer to grandma and grandpa with kids?

Or will you want to expand your home by finishing the basement and building an addition?

What are the school districts like in your neighborhood?

In any of these circumstances, it may make sense to buy a fixer upper in an up-and-coming neighborhood or it may make sense to save your money and rent for now, so you’ll be free to move when the time comes.

Rent vs. Buy vs. Wait

I think you get it by now.

Oftentimes, it’s not a question of what is better: renting or buying a home.

More specifically, the question is: Is it better to rent or to buy right now?

I think this is where a lot of the confusion and anxiety comes in. Buying a home is often seen as a momentous step toward stability and settling down. (Unless you’re specifically buying a home to flip it.) Deciding to buy a home means you have to have all that sorted out. Where are you going to be living in the next 30 years? Who will you be living with? Where will you work? What is the rest of your life going to be like?

If you don’t have those questions answered, then honestly, maybe renting is your best bet.

Unless…

You just know in your heart of hearts that you want to be a homeowner. If you are here because you’re looking for justification for your desire to buy a home, then stop looking. You don’t need justification, financial, logistical, or otherwise. You should certainly consider these things, but at the end of the day, the decision to buy a home is an emotional one. It’s a personal choice you make, and all the arithmetic in the world can’t quantify your feeling of satisfaction and pride in owning a house.

Whether you rent or buy, you should keep your end goal in mind and make sure your next step is in that direction. This might mean renting for now, while you wait for the market to cool down or the perfect property to go up for sale. Or it might mean buying a starter home that you’ll enjoy fixing up on the weekends.

The last thing you should do is to assume that either choice is throwing money away. Whether you’re renting space from a landlord or renting money from a bank, you’re making a purchase. You’re paying for a place to live, and that’s a necessity.

Do what makes sense for you. Focus on how you want to live your life, not how you feel like you should be living your life, and make your decision based on that.